The recurring theme as of late is appraiser pressure.

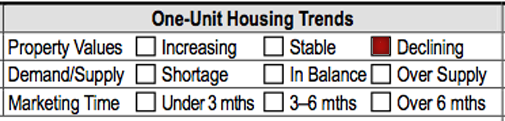

Near the top of all the various appraisal forms designed by Fannie Mae, considered the standard by the residential mortgage industry, is the “neighborhood” section. It contains a series of check boxes that appraiser uses to identify the overall trend of the neighborhood where the subject property is located.

An appraiser in California is suing Washington Mutual Bank, the embattled mortgage lender who is under regulatory investigation by the Office of Thrift Supervision after the New York State Attorney General initiated a law suit against one of their primary appraisal vendors. The appraiser was supposedly blacklisted by WaMu for checking the “declining” box on her appraisal forms, because she observed price declines in the market she was covering.

The action is surprising to me since appraisers are usually the recipients of punishment. The appraiser is hired to render an opinion about the local housing market. Based on the lawsuit, this appraiser was not allowed to present her opinion without retribution. Kudos to her. The typical new type of appraiser born out of the housing boom, would not have checked that box and that makes me angry.

This was my comment to the Wall Street Journal about this last week.

>Jonathan Miller, a New York appraiser, said pressure on appraisers not to check the “declining” box in their reports is widespread and that many appraisers submit to such demands. But “if you do that,” he says, “you’re not doing an appraisal anymore — you’re a form-filler.”

I always viewed these check boxes as an “on/off switch” and ethical appraisers that would check these boxes were placed at high risk to lose their retail banking clients because those clients had to sell the mortgage paper to investors. There was generally less concern about banking clients that held the reports in portfolio.

Fannie Mae released policy guidance last year that would cut back the allowed mortgage by 5% if this check box was selected. It is logical for Fannie Mae to implement this policy since it is an underwriting decision whether or not to lend or how much to lend in a market. The appraiser is merely the observer and the valuation expert, and the appraiser has nothing to do whatsoever with making underwriting decisions for the lender.

On the other end of the spectrum, I remember getting calls about not checking the “Increasing” box when the market began to rise in the late 1990s so as to be more conservative. Of course we would decline the instruction explain how we could not implement the request without a full disclosure and disclaimer. We found that most of the other appraisers on the approved panel of that same bank, would readily agree to the lender instructions without resistance.

Where was our profession’s backbone? Good grief.