This quarterly market report is provided by Dr. Kevin Gillen, an economist at the Real Estate Department of the Wharton School and Fellow of the University of Pennsylvania. He analyzes the Philadelphia real estate market using the city’s real estate database through Econsult, an economics consulting firm based in Philadelphia PA that provides statistical & econometric analysis in support of litigation as well as business and public policy decision-makers. His results are published in a research paper called Philadelphia House Price Indices each quarter as a public service to the Philadelphia real estate community. Here’s his methodology [pdf].

Kevin does a great job parsing out the market and it is a pleasure to share his results on Matrix —Jonathan Miller

Download the full report [pdf].

Read Kevin’s analysis: Philadelphia’s Housing Market Deteriorates Sharply in Q1: But city now considered “under-valued” for the first time since 2003.

>According to the latest analysis by Wharton and Econsult economist Kevin Gillen, the typical

Philadelphia home fell in value by an average of 8.4% on a quality- and seasonally- adjusted

basis this past winter. This is an accelerated rate of decline from previous quarters. And, when

added to previous price declines, Philadelphia house values are down cumulatively by 17.1%

from the local market’s peak of nearly two years ago.

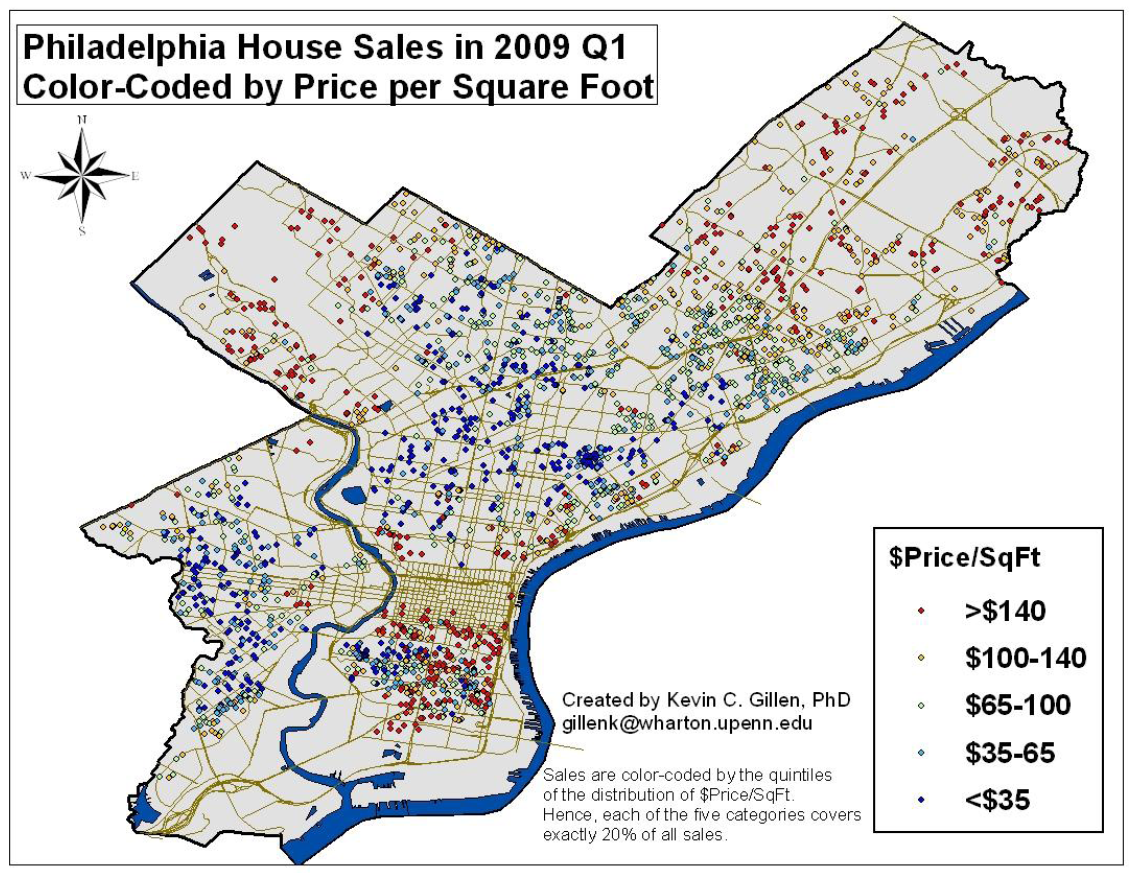

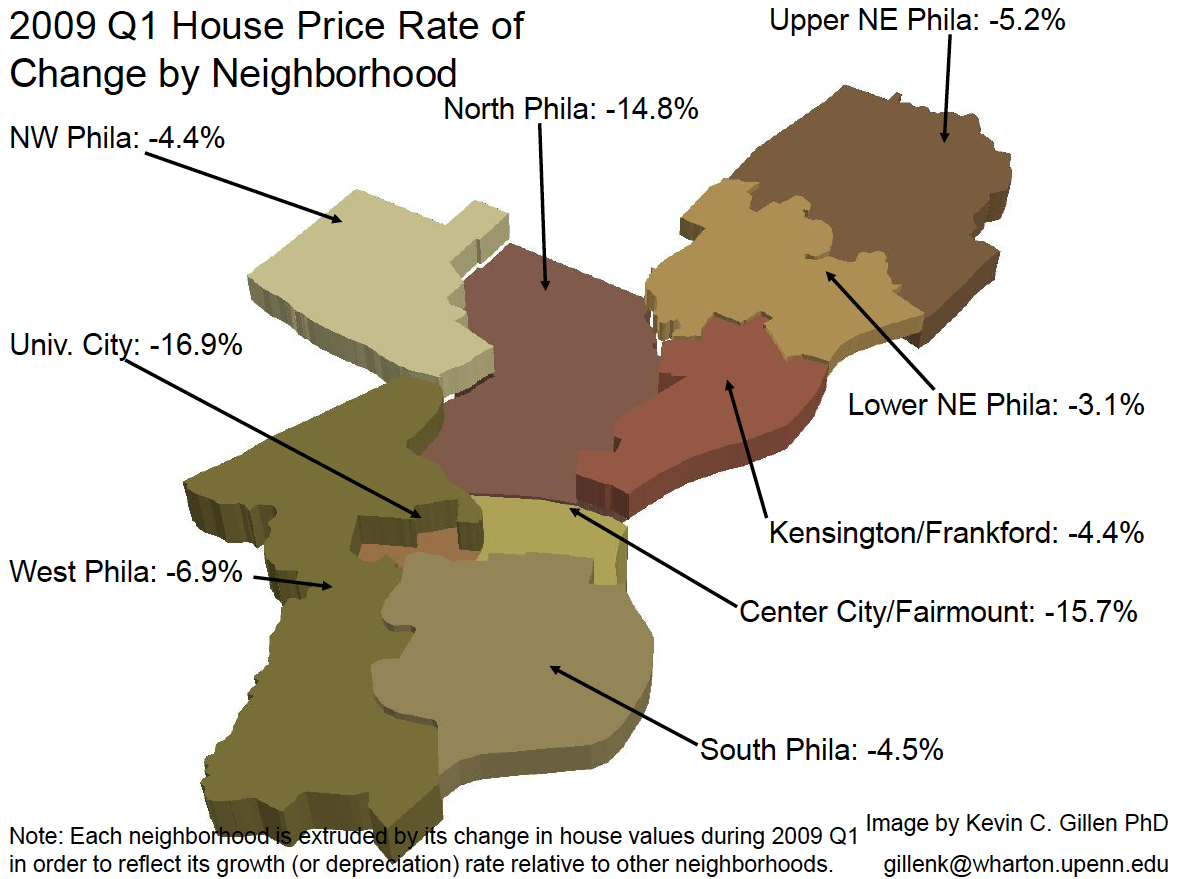

* Price changes across the city’s neighborhoods were uniformly negative, with no areas exhibiting

any price appreciation.

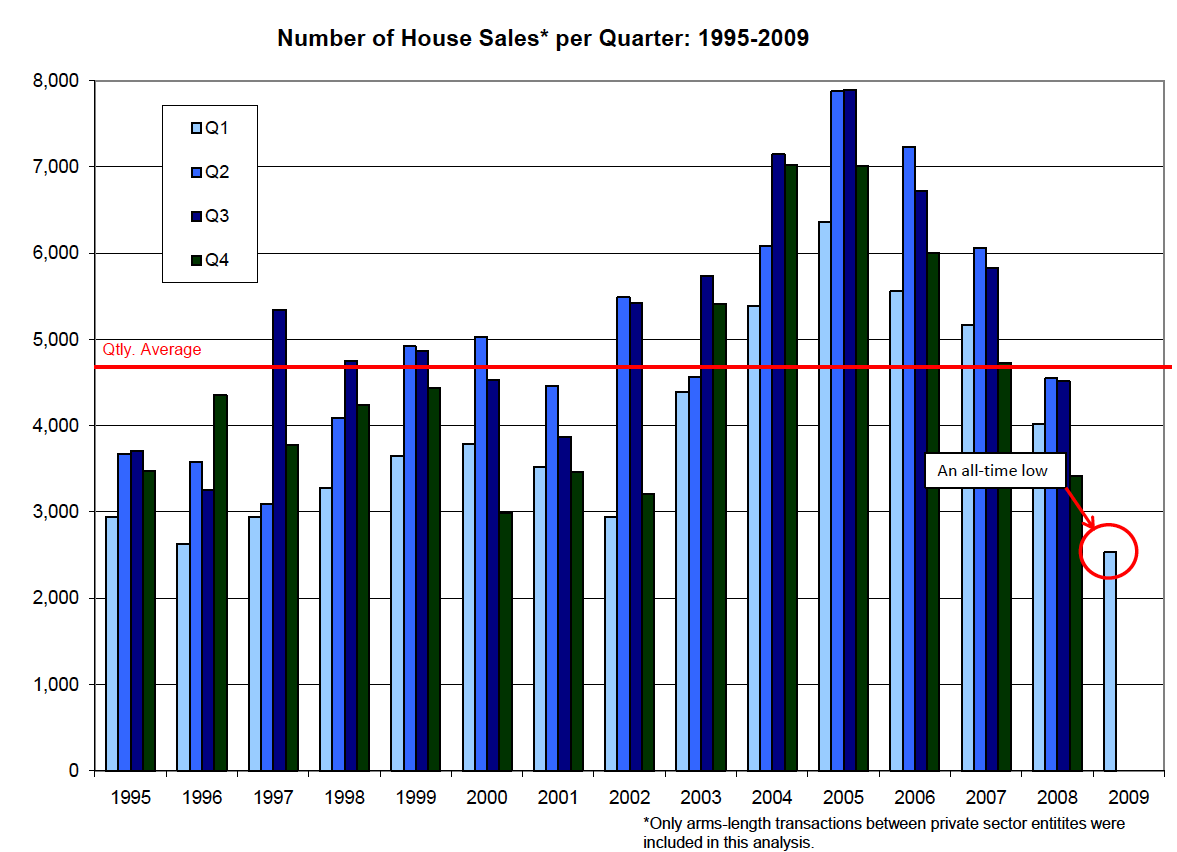

* According to the data, 2,530 homes transacted under arms-length conditions this past winter; an

all-time low.

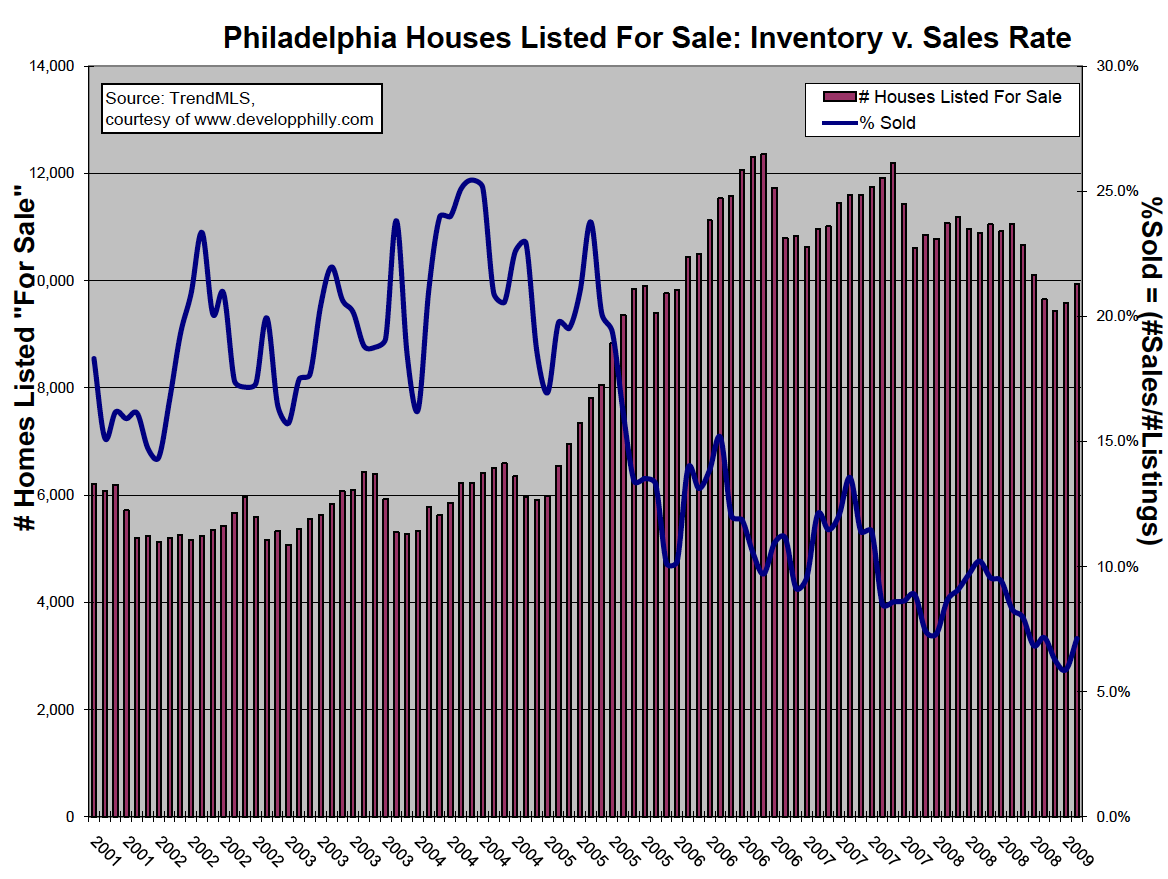

* …it still seems to out-perform its peers in its relatively low foreclosure rate.

* Philadelphia’s housing is now actually considered to be under-valued.

3 Comments

Comments are closed.

Did I miss something or is Prof. Gillen unaware that debt bubbled up and then blew up? I read through his papers and I can’t find any index component in his housing price studies that speaks to available funds.

How can he declare housing is under-valued when the cause of a decrease in prices and activity is due primarily to lender shenanigans? He seems to treat housing prices as if the only scenario is business as usual.

It’s more or less the relationship of income and housing values.

OK. I can’t find his reference to income, but if you say it is there then so be it. My question still remains, although including income in the equation ties the conclusion of under-value to something other than the housing market itself (i.e. the average didn’t go up as much as the trend would indicate), is there any comparison to other essential components of effective demand such as the availability of mortgage loans?