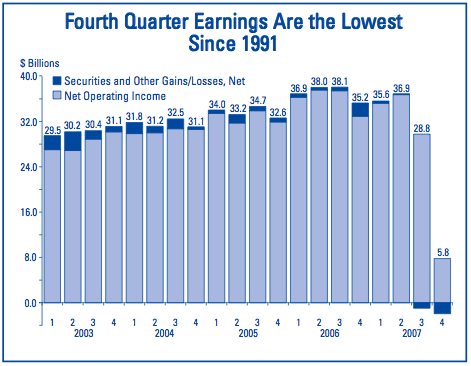

Bank earnings are down.

Way down.

Real concerns about future losses from non-performing mortgages, other credit instruments like credit cards and the need to recapitalize.

Fed policy has been pretty generous to the economy, no?

No.

Current hopeful scenario: Lower the federal funds rates a lot so that banks can lower mortgage rates to enable consumers to refi their way out of trouble for the time being or purchase a new home.

Looked good on paper…

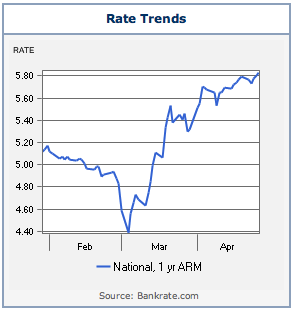

But mortgage rates have been rising, whether it’s a jumbo or conforming, fixed or adjustable.

Banks need to recapitalize because they have been forced to lend and hold the mortgages they issue in their own portfolio.

>Borrow at a low rate,

lend at a high rate.

Enjoy the spread.

Banks can lend at a higher rate because fewer banks are lending so there is less competition. In addition, the banks that are still lending have much tighter underwriting requirements compared to the past 3-4 years.

Why? Banks now have to be more accountable for risk in their mortgage lending decisions rather than offloading risk to investors, who would in turn offload the risk to other investors and so on.

It’s all about the credit markets. Until they begin to function again, banks will not be incentivized to offer lower the rates on mortgages they issue.

This is another form of “bailout.” The Fed is keeping the banking sector from imploding (opposite of spreading – very lame, sorry).

2 Comments

Comments are closed.

bingo JM! Hence why 3Mth LIBOR is 65+ bps above fed funds rate, as banks are still risk adverse.

Credit markets are experiencing big time short covering and some bottom feeding right now, bring some liquidity and bids back to these illiquid marketplaces. That is giving a false sense of hope. It doesnt change housing issues, debt issues, spread of problems from subprime to alt-a, prime, option arms, cosi/cofi, credit cards, etc..

If we truly experienced the worst already, then man, the fed did an amazing job. I just doubt that. We need LIBOR to get back within 10-15 bps of ffr and Ill be convinced that credit markets are behaving better

Wait, I thought the saying was, if you were a banker:

Borrow at 8

Lend at 10

Be on the links by 2